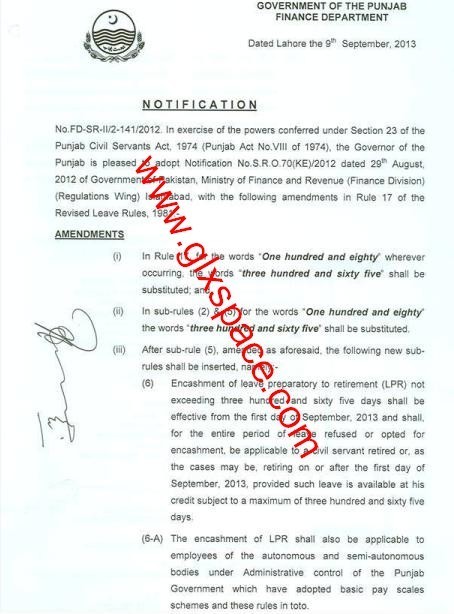

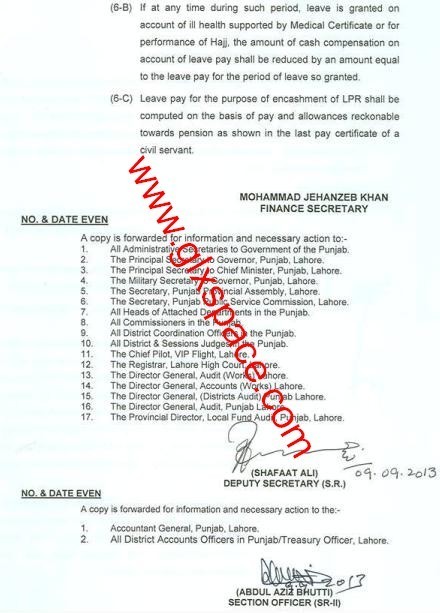

When an employee is retired from Govt service on the basis of Encashment, the encashment of leave is due for the said employee. This encashment is granted to the employee on the leaves in his/her credit not exceeding to 365 days according to new rules of encashment of 2012. The greater the number of leaves in his/her credit the more encashment he/she will get.

An employee can avail encashment after the minimum service of 30 years or the employees can avail encashment at the age of 60 years. The pay is calculated that he/she was being drawn during the period of last days i.e if an employee has 200 days leave in his/her credit then the pay of last 200 days is calculated for the encashment purpose. The formula for the purpose of calculating encashment of leave is as under:

Basic Pay x 5.918 x Leaves in credit/180

Note this formula is before the revision of leave encashment from 180 to 365 days. New formula will soon be replaced.

How to Calculate Leave Encashment manually

I will illustrate you with example that how to calculate the leave encashment manually. Suppose a person has 60 days leave in his/her credit at the time of retirement. He/she retired on 08/01/2013 with basic pay Rs. 15000 while his/her pay was 13000/- before 1st December 2012. We will go back 60 days from 08-01-2013 in this way and will make the calculation of encashment in this way:-

| Period | Days | Pay | Amount |

| January 2013 | 08 Days | 15000/- | 3871/- |

| December 2013 | 31 Days | 15000/- | 15000/- |

| November 2013 | 21 Days | 13000/- | 9100/- |

| Total | 60 Days | 27971/- |

Don’t Miss: Notification of Encashment of Leave 2012